😻 | The Pet Industry's Quiet Pivot: Why "Demographics Is Destiny" Is About to Reset Everyone's Plans

Source: Catalyst Council, Jeff Mard, Claude & Chat GPT

For five years, the U.S. veterinary industry has told itself a comforting story: clinical visits dipped after the pandemic, but they'll snap back to the familiar 2% to 3% annual growth any quarter now. A new white paper says that story is, in the authors' own framing, probably wishful thinking — and the data behind it is hard to argue with.

The report (download here), Puppocalypse, Kitten Craze, and the Expectations Reset: What Pet Demographics Reveal About U.S. Veterinary Visits Through 2035, was published June 11, 2026 by the CATalyst Council, co-authored with Vetsource and Kynetec. Its authors — Jon Ayers, Gina Fortunato, Kristin Wuhrman and Jane Brunt of CATalyst Council, Jim Hansbauer of Vetsource, Stephanie Crisp of Kynetec, and David Kincaid of Dedekind Cut Labs — set out to test the industry's conventional wisdom against the raw demographics of who is actually walking through the clinic door. What they found is the beginning of a considerable pivot, one most operators haven't priced in yet.

Two opposite stories, one species at a time

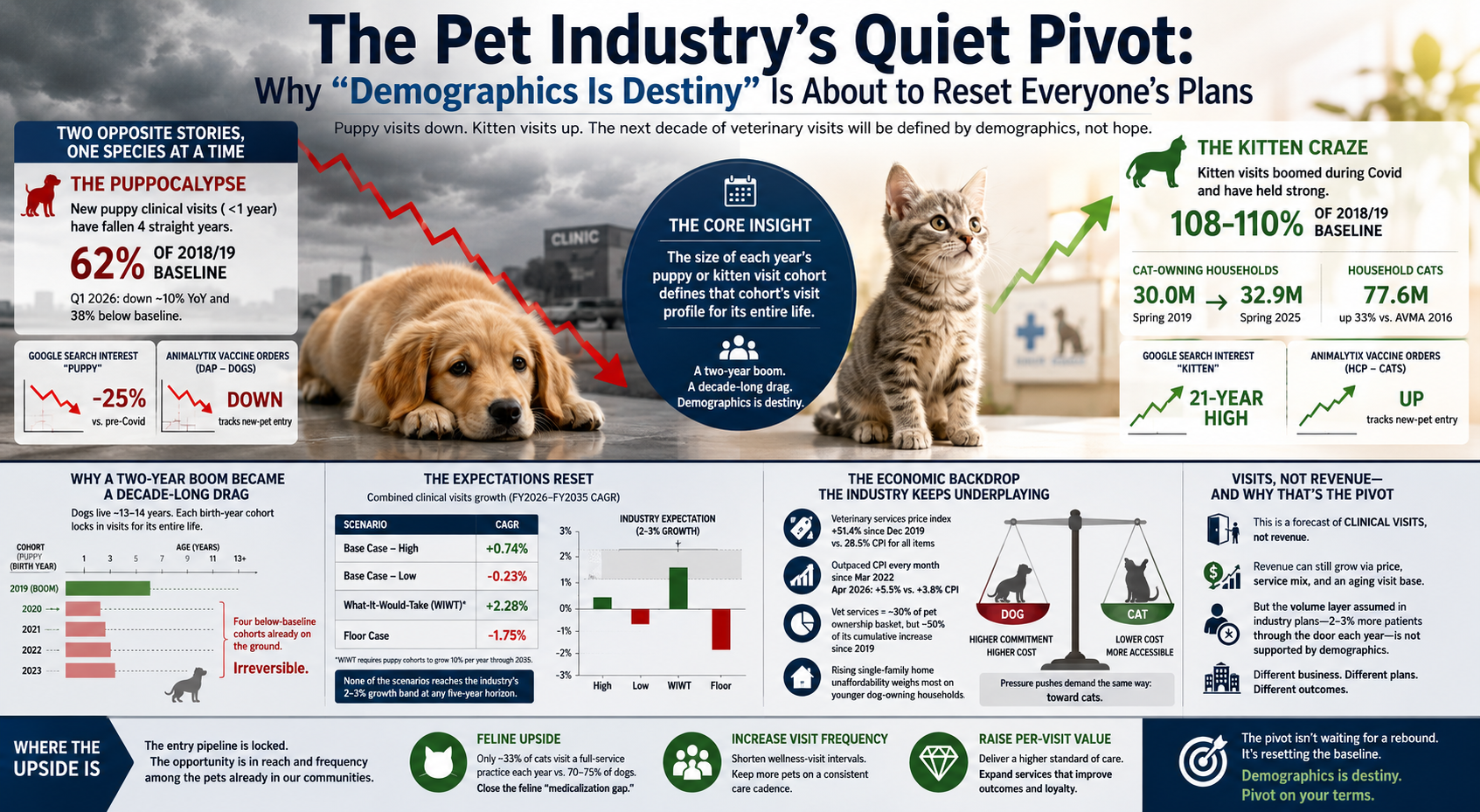

Start with the headline divergence. According to the report, new puppy clinical visits — patients under one year of age — have fallen for four straight years since the Covid boom, landing at roughly 62% of the 2018/19 baseline, the last "normal" years before the pandemic. The authors give this its own name: the Puppocalypse. By Vetsource's Q1 2026 reading, puppy visits were down about 10% year-over-year and sitting 38% below baseline.

Cats are doing the opposite. Kitten visits boomed during Covid and then held, running 8% to 10% above the 2018/19 baseline for four consecutive years — the Kitten Craze. The structural support is real: per the report, cat-owning households grew from 30.0 million in Spring 2019 to 32.9 million in Spring 2025, and the 2026 CATalyst Council State of the Cat survey counted 77.6 million household cats, up 33% from the last large-scale AVMA count in 2016.

Two independent signals corroborate the split. Google search interest for "puppy" has fallen roughly 25% below its pre-Covid level, while "kitten" interest has reached a 21-year high. And Animalytix vaccine ordering data — DAP doses for dogs, HCP for cats, both given mostly to young animals — tracks the same divergence in new-pet entry.

Why a two-year boom became a decade-long drag

Here's the insight that makes this more than a passing slump. The report's central, empirically grounded observation is that the size of each year's puppy or kitten visit cohort defines that cohort's visit profile for its entire life. A small birth-year class enters small and stays below baseline as it ages, year after year, across the roughly 13-to-14-year life of a dog.

That asymmetry is the whole game. The puppy boom lasted two years. But there are now four consecutive below-baseline puppy cohorts already on the ground — and no future recovery in puppy numbers can undo cohorts that have already entered. As the authors put it, the boom was a two-year event; the Puppocalypse is four years, confirmed, and counting. The visits those missing puppies won't generate as adults are already baked into the next decade.

The report builds its forecast by stacking each birth-year cohort onto an observed "visit attrition curve" and aging it forward. The arithmetic is unsentimental. Because canines carry roughly 77% of combined clinical visits and new puppy entry now runs well below the rate at which older dogs leave the visit pool, the math points down. The sustained Kitten Craze only partly offsets it, because cats contribute less than a third of canine visit volume.

The expectations reset

This is where the pivot lives. The prevailing industry narrative — shared across corporate practice groups, diagnostics makers and pharma manufacturers — assumes clinical visits return to 2% to 3% growth within a few years. The CATalyst Council's replacement-rate logic instead puts combined visit growth at -2.0% to 0.0% through 2030.

The report runs four scenarios, distinguished only by assumptions about future puppy and kitten cohort sizes. The combined FY2026–FY2035 compound annual growth rates tell the story:

Base Case – High: +0.74%

Base Case – Low: -0.23%

What-It-Would-Take (WIWT): +2.28%

Floor Case: -1.75%

Even the optimistic base case doesn't return to visit growth until around 2030 — not the near-term rebound the industry expects. And the only scenario that approaches the industry's 2-to-3% band, the "What-It-Would-Take" case, requires puppy cohorts to grow 10% per year through 2035. For context, the report notes the only year in history that puppy visit growth exceeded 4% was the first year of the Covid boom, at 13%. The authors built WIWT not as a forecast but to show how implausible the assumptions behind the conventional wisdom really are. None of the three growth scenarios reaches the 2-to-3% band at any five-year horizon.

The economic backdrop the industry keeps underplaying

The demographic engine has an economic backstory, which the report treats carefully as a candidate contributor rather than a proven cause. The standout figure: per the U.S. Bureau of Labor Statistics, the veterinary services price index has risen 51.4% since December 2019, against 28.5% CPI for all items. Veterinary prices have outrun headline inflation every month since March 2022 and still ran 5.5% year-over-year in April 2026 versus 3.8% CPI. Within the total cost of pet ownership, veterinary services are roughly 30% of the basket yet account for close to half of its cumulative increase since 2019.

That pressure falls hardest on the higher-commitment animal — the dog — while the cheaper, apartment-compatible cat absorbs less of it. The report pairs this with rising single-family home unaffordability, which weighs on the younger generations most likely to take on a dog. Both forces, the authors note, push demand the same way: toward cats.

Visits, not revenue — and why that distinction is the pivot

The most important strategic point in the paper is also its most easily missed. This is a forecast of clinical visits, not revenue. And the industry's growth algorithms are ultimately revenue algorithms, with visit volume sitting beneath price and service mix.

The authors are explicit that they are not claiming veterinary revenue can't grow 2% to 3%. Price realization, a richer service mix, and an aging visit base that skews toward higher-value senior and sick-animal care can carry revenue above the visit-volume path. The narrower — and, they argue, more consequential — claim is that the volume layer those revenue algorithms quietly assume, 2% to 3% more patients through the door each year, is not supported by the demographics.

That is a materially different business. A practice riding a rising tide of patients plans very differently for capacity, staffing, real estate, and the durability of same-store growth than one whose patient count runs flat to negative while revenue leans on price and mix. Plans underwritten by the old assumption are, quietly, planning for a world that the entry pipeline no longer produces.

Where the upside actually is

The report doesn't end in fatalism — it ends in a lever. Because demographics is destiny on the entry side, the actionable upside lives in reach and frequency among the pets already out there.

The clearest opportunity is feline. Only an estimated 33% of household cats visit a full-service practice in a given year, versus 70-75% of dogs — what the authors call the feline "medicalization gap." The aggregate visit mix is already shifting toward cats, with feline share of combined clinical visits projected to climb from about 20% toward the mid-20s by 2035. Effective, feline-specific marketing that brings even a few more of those uncounted cats through the door is pure upside the forecast doesn't assume. So is shortening the wellness-visit interval for existing clients, or raising the standard of care per visit.

In other words, the entry pipeline is largely locked. What practices and groups still control is how many of the pets already in their communities get seen, and how often.

The takeaway

The pivot the CATalyst Council is describing isn't a downturn to wait out — it's a reset of the baseline assumption underneath an entire industry's planning. As the authors put it, the forecast rests on demographics, and demographics is destiny. The four below-baseline puppy classes already on the ground will shape canine visit volume for the next decade no matter what happens next, while cats quietly become a larger and more important share of the room.

Operators who internalize that early — shifting from a volume-growth mindset to one built on feline reach, visit frequency, and per-visit value — will be the ones who pivot on their own terms rather than having the demographics do it for them.

Source: CATalyst Council, in collaboration with Vetsource and Kynetec, "Puppocalypse, Kitten Craze, and the Expectations Reset: What Pet Demographics Reveal About U.S. Veterinary Visits Through 2035," June 11, 2026. Underlying data drawn from Vetsource clinical visits by age, Kynetec PetTrak, IDEXX Practice Intelligence, Animalytix State of the Industry, the 2026 CATalyst Council State of the Cat survey, U.S. Bureau of Labor Statistics CPI for veterinary services, and Google Trends.